Summary

- Moody’s downgraded China to A1 from Aa3 and changes outlook to stable from negative

- Downgrade combined with increased regulations means a hit to international M&A, but there may be a silver lining for the mid-market

China is downgraded

On May 24, 2017 Moody’s downgraded China’s sovereign credit rating— the nation’s first downgrade since 1989. Moody’s downgraded China’s rating to A1 from Aa3, reflects Moody’s is concerning about the economy-wide debt continuing to rise as potential growth slows.

In 2016, corporate debt in China was approximately 1.7x GDP, while their total debt, which includes corporate debt, government debt, business debt and household debt, was about 2.6x GDP. Moody’s expects China’s total debt to GDP ratio to continue to increase. We would also assume the mounting debt problems in China would influence future M&A activities.

The Effect on Mergers and Acquisitions (M&A) from China

Throughout the past few years, Chinese companies have extended their acquisition reach to virtually every corner of the world. In 2013, Chinese government announced “Going Out” Overseas Investment Strategy to encourage the globalization of domestic enterprises. Supported by the government, Chinese companies became able to execute large deals, especially in technology industry.

This has the possibility to boost M&A activities in the mid-market segment. In contrast to large $1B+ transactions, the smaller size of mid-market transactions generally means less reliance on corporate debt. Mid-market deals closed in all cash will not be more difficult for Chinese regulators to oversee.

Actually, active purchasers in IT industry, including Alibaba Group, Tencent Holdings Limited and Baidu, Inc., are continuing receiving supports from the Chinese government. Meanwhile, other Chinese companies are increasingly interested in investing in US-based technology companies. We expect this trend to continue.

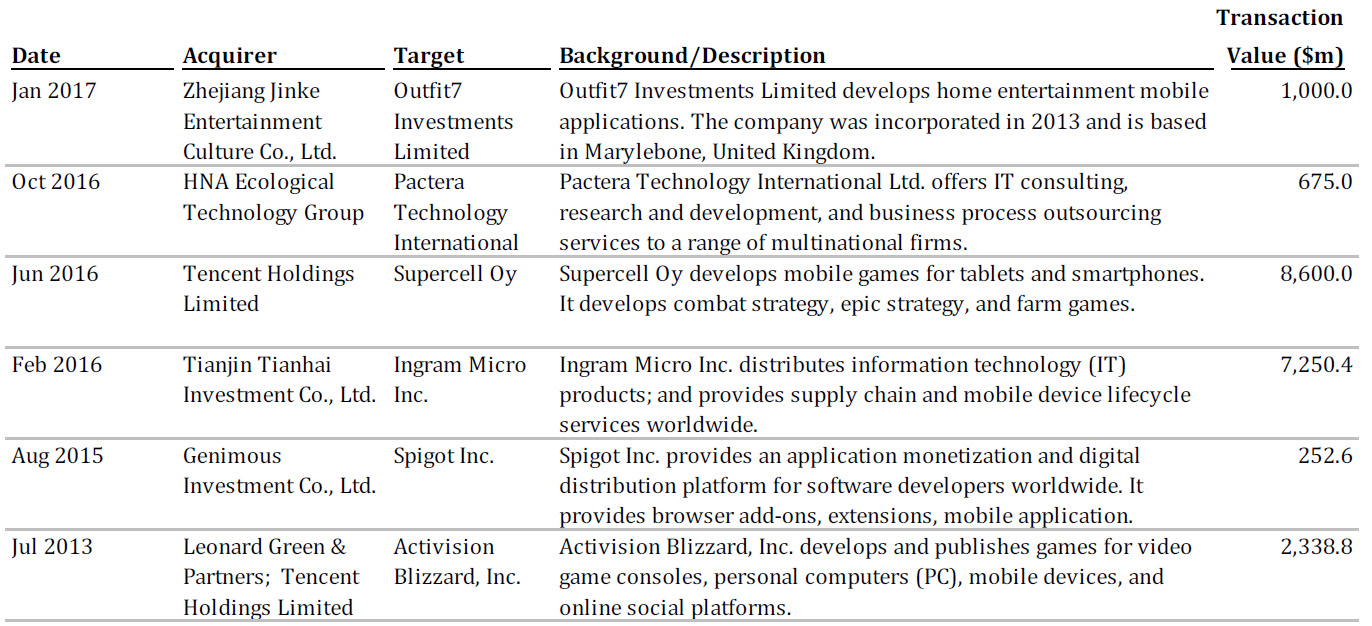

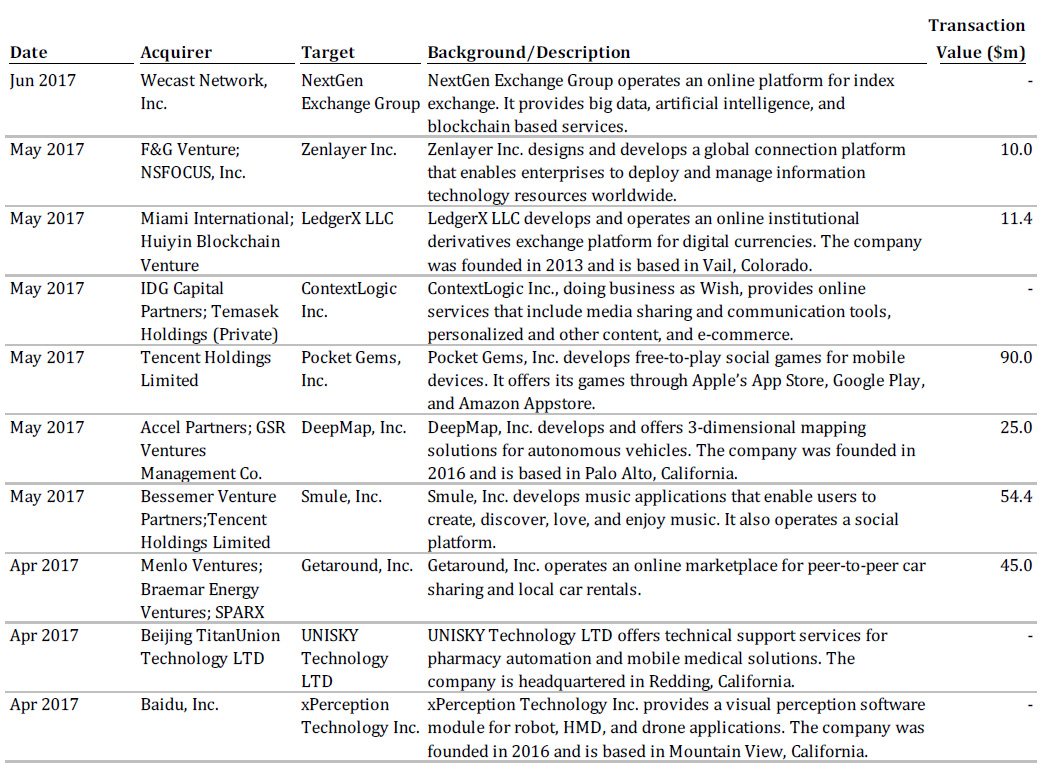

Recent Acquisitions and Investments in the U.S. Mid-Market Tech Segment from China

True Blue Partners is a M&A advisory firm that serves lower mid-market enterprise software and service companies. For more information please visit www.truebluepartners.com or email us at info @ truebluepartners . com